From Inputs to Infrastructure: Where the System Actually Breaks

By Eric Greene (Greene Financial Advisory) & CedarOwl

This piece brings together two complementary perspectives—

Eric Greene, focused on capital flows and real-world infrastructure, and CedarOwl, whose work centers on synthesizing geopolitical and macro frameworks across global markets.

In a recent piece, I highlighted rare earth processing as a critical bottleneck. What’s becoming clearer is that this isn’t isolated—it’s part of a broader pattern now emerging across industrial systems.

There’s a tendency to frame the current environment as a series of supply problems.

Rare earths. Helium. Fertilizers. Petrochemicals.

Each gets analyzed on its own terms.

But that framing misses what’s actually happening.

This isn’t about isolated shortages. It’s about a system under strain—one where the pressure is building not at the source, but across how inputs are processed, connected, and ultimately turned into something usable.

Because having something in the ground has never been the same as being able to use it at scale.

Where the System Actually Breaks

Most analysis still begins upstream—where the resources are and who controls them.

Important questions—but incomplete.

The constraint isn’t geological. It’s industrial.

It shows up later—where materials have to be refined, separated, and converted into functional inputs. That’s where timelines stretch, costs rise, and dependencies become far more concentrated than most assume.

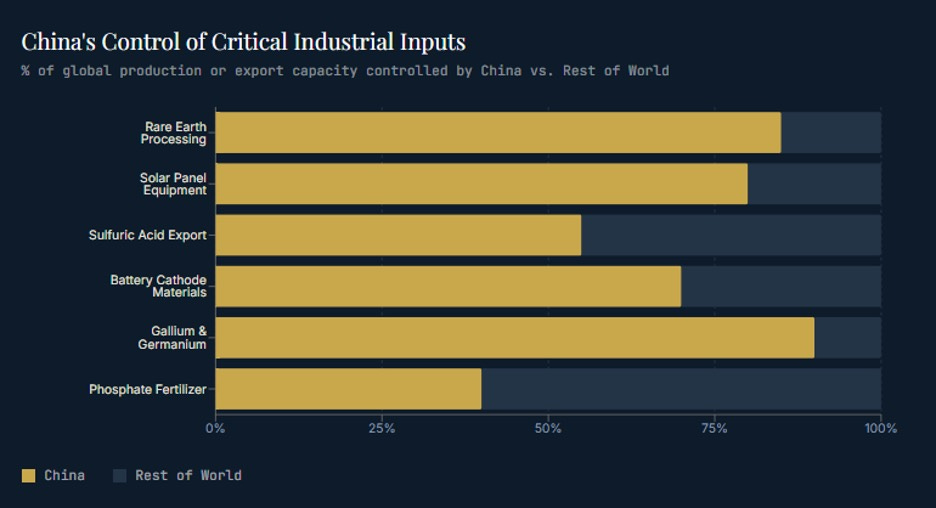

In some cases, that concentration isn’t just high—it’s effectively absolute.

China’s position across key industrial inputs reflects this clearly:

This isn’t just market share. It’s control of the conversion layer—the point where raw materials become usable.

The Invisible Chokepoint

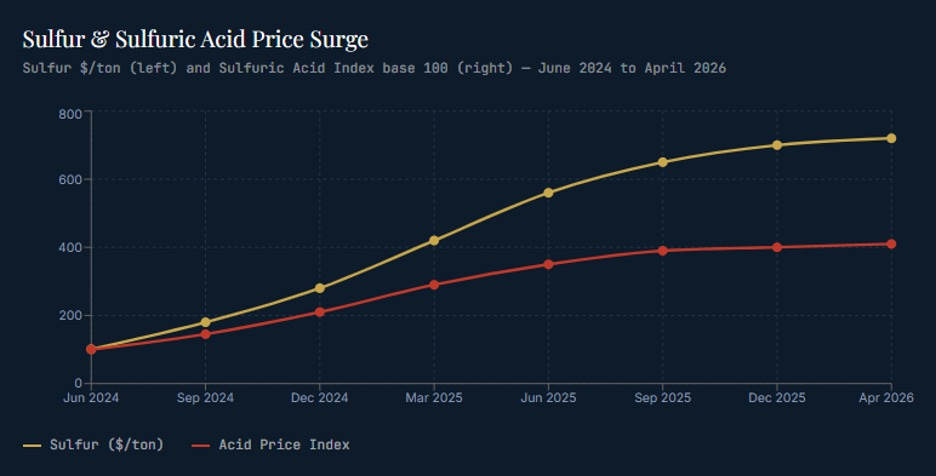

One of the clearest examples of this dynamic is something most people never think about: sulfuric acid.

It sits at the center of industrial production—critical for copper extraction, nickel processing, and phosphate fertilizers that support global food systems.

And right now, it’s tightening.

China is restricting exports, while disruptions through the Strait of Hormuz are pressuring sulfur flows from the Middle East—historically a major source of supply.

Individually, those developments matter.

Together, they compound.

Sulfur prices have already moved from roughly $100 per ton in 2024 to over $700 in some markets—feeding directly into mining costs and production decisions.

This is how pressure builds:

Input costs move

Production economics shift

Supply chains adjust

And once that process begins, it rarely stays contained.

From Efficiency to Fragility

For decades, the global system optimized for efficiency.

Production moved to where it was cheapest. Processing followed. Supply chains stretched across borders under the assumption they would remain intact.

For a long time, that worked.

But it also created fragility—less visible, but far more consequential.

Not at the source, but in the middle of the chain, where materials are transformed and made usable.

That’s where disruptions don’t just slow things down—they force the system to adapt.

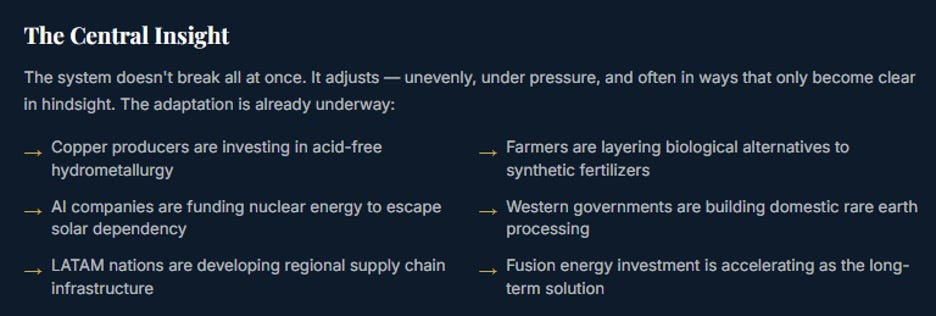

How Systems Actually Adapt

Finance blogger and author Charles Hugh Smith has developed the S-curve of Systemic Adaption:

That adaptation doesn’t happen through simple substitution.

It happens through layering.

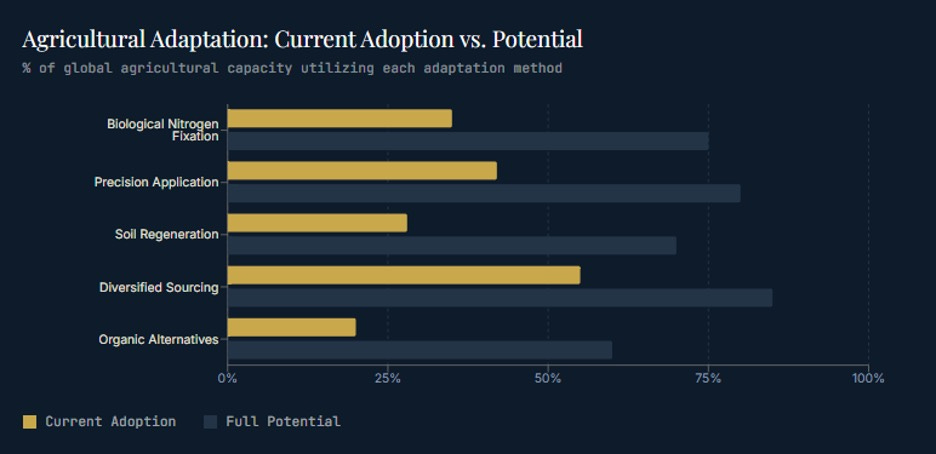

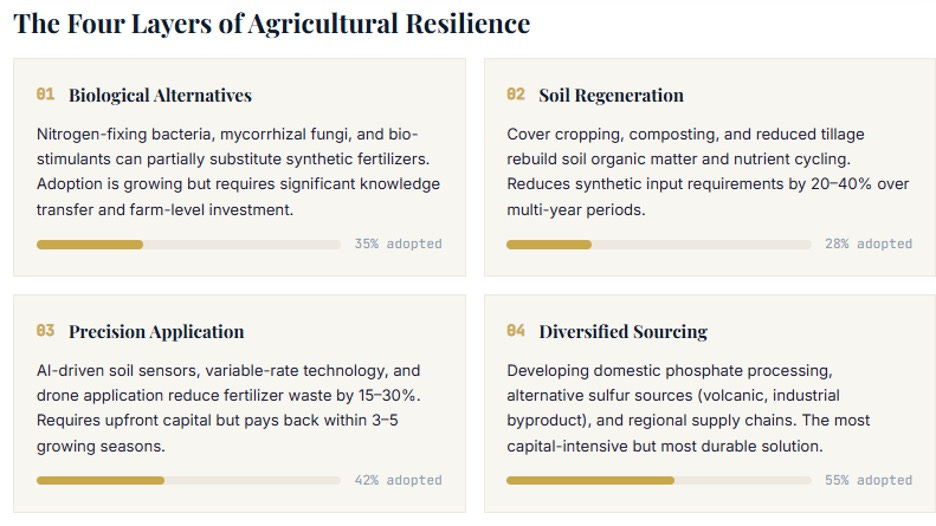

You can already see this clearly in agriculture, where fertilizer supply—particularly nitrogen-based inputs—has long been concentrated in specific regions.

When that flow is disrupted, the response isn’t to replace one input with another.

It’s to build a more resilient system:

The system becomes more complex—but also more durable.

This is the pattern that repeats across sectors.

A critical input tightens.

Costs move.

Dependencies are exposed.

And the system reorganizes—toward redundancy, regionalization, and resilience.

A Broader Reordering

This dynamic isn’t happening in isolation.

It’s unfolding within a larger geopolitical shift.

As Zoltan Pozsar has framed it, the United States is increasingly focused on controlling energy and financial chokepoints, while China continues to consolidate control over industrial processing and manufacturing capacity.

The result isn’t a traditional trade conflict.

It’s a structural standoff—one where both sides are targeting the layers of the system the other depends on most.

And neither can unwind those dependencies quickly.

Where This Leads

What we’re witnessing isn’t a temporary disruption.

It’s the early stage of a broader reorganization of the global industrial system.

One that moves away from:

centralized efficiency

And toward:

distributed resilience

regional infrastructure

layered supply chains

The adjustment won’t be linear.

It will be uneven, and at times abrupt—showing up first in costs, then in production, and eventually in how entire systems are designed.

Closing Perspective

The system doesn’t break all at once.

It adjusts—under pressure, in layers, and often in ways that only become clear in hindsight.

Understanding that process—where it starts, how it spreads, and how it resolves—is where both analysis and opportunity begin.

— Eric Greene

Founder, Greene Financial Advisory

Founder & Chief Architect, TCE12 Corridor Initiative

— CedarOwl

Geopolitical Strategist & Macro Analyst

Disclaimer: This information and material contained in this post is of a general nature and is intended for educational purposes only. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. This post does not constitute a recommendation or a solicitation or offer of the purchase or sale of securities. Furthermore, this post does not endorse or recommend any tax, legal, or investment related strategy, trading related strategy or model portfolio. The future performance of an investment, trade, strategy or model portfolio cannot be deduced from past performance. As with any investment, trade, strategy or model portfolio, the outcome depends upon many factors including: investment or trading objectives, income, net worth, tax bracket, suitability, risk tolerance, as well as economic and market factors. Economic forecasts set forth may not develop as predicted and there can be no guarantee that investments, trades, strategies or model portfolios will be successful. All information contained in this post has been derived from sources that are deemed to be reliable but not guaranteed.