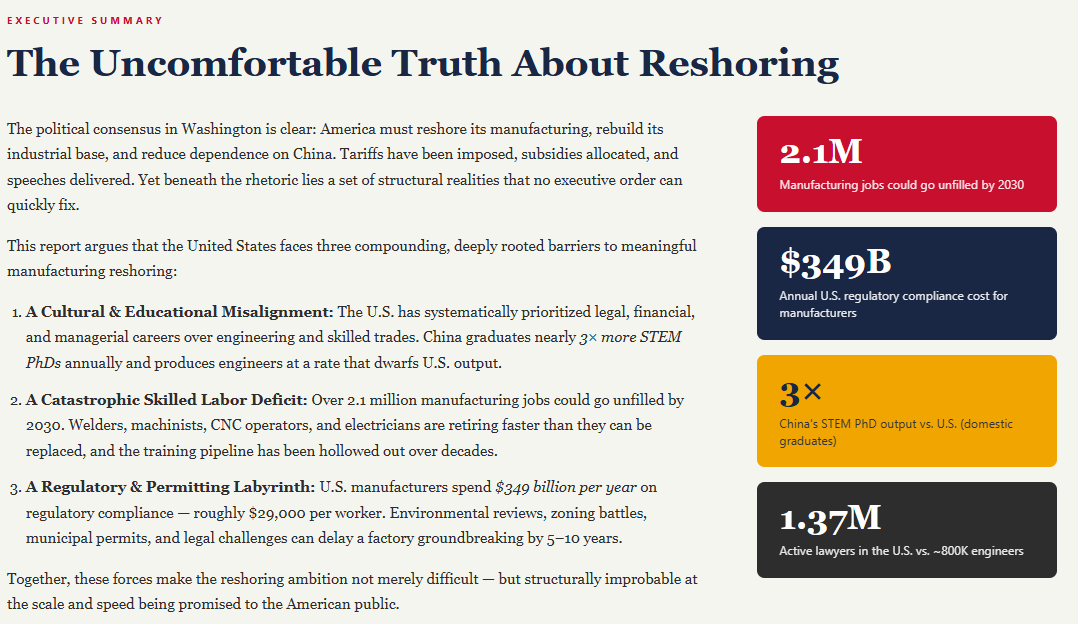

The Reshoring Illusion

Why America Cannot Rebuild Its Manufacturing Base: Lawyers, Regulations and the Skills Deficit

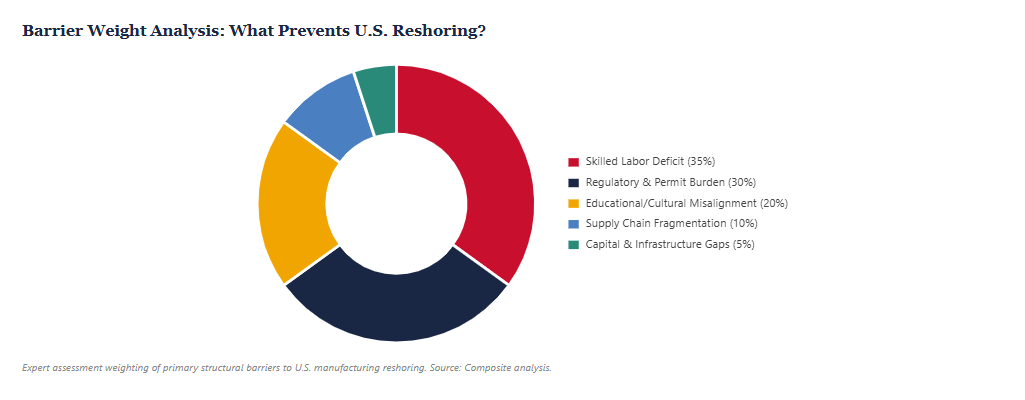

This week we explore with charts and other data points why America cannot rebuild its manufacturing base.

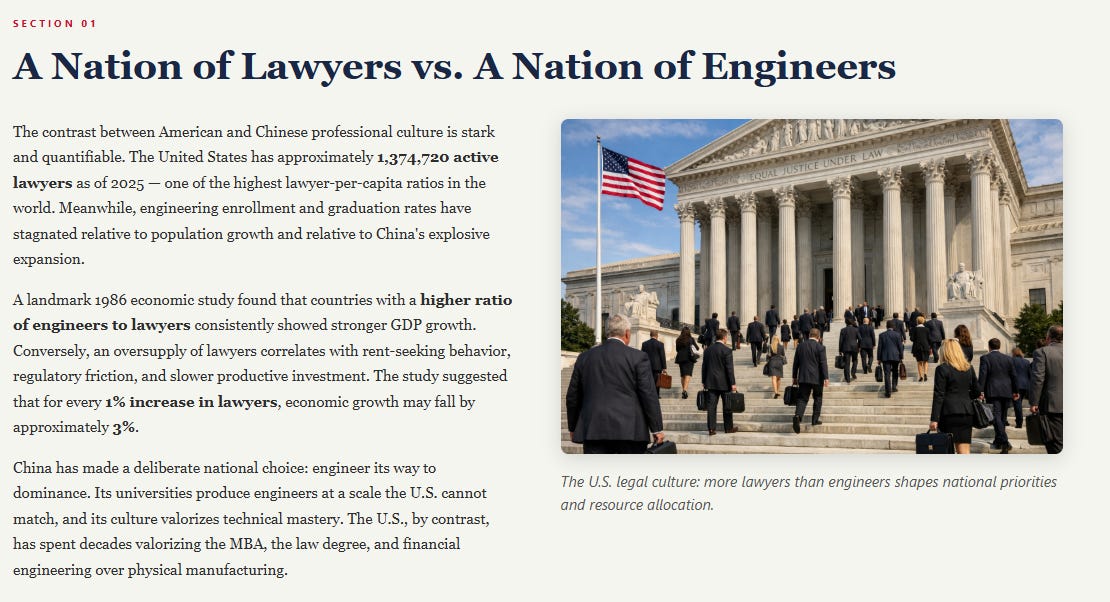

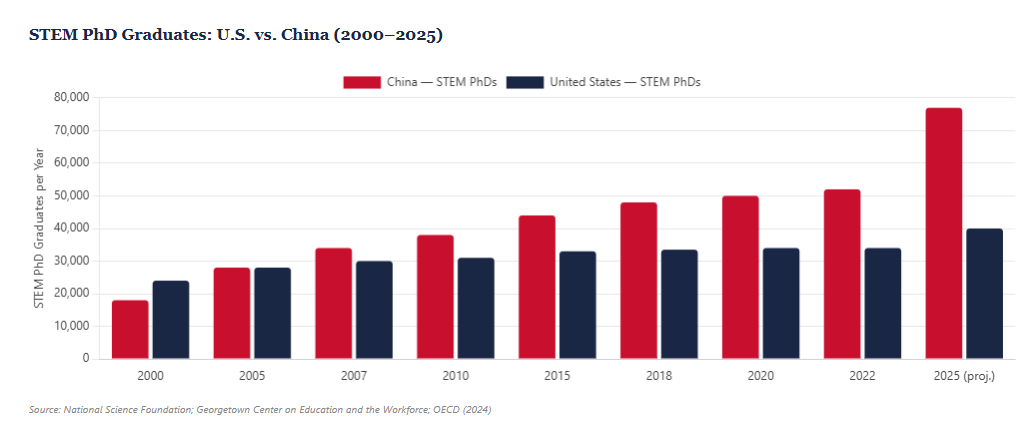

Key Finding: By 2025, China will award roughly double the STEM PhDs of the United States. If international students are excluded from U.S. counts, Chinese graduates outnumber U.S. domestic graduates by more than 3 to 1. The U.S. is not losing a race — it has already lost it.

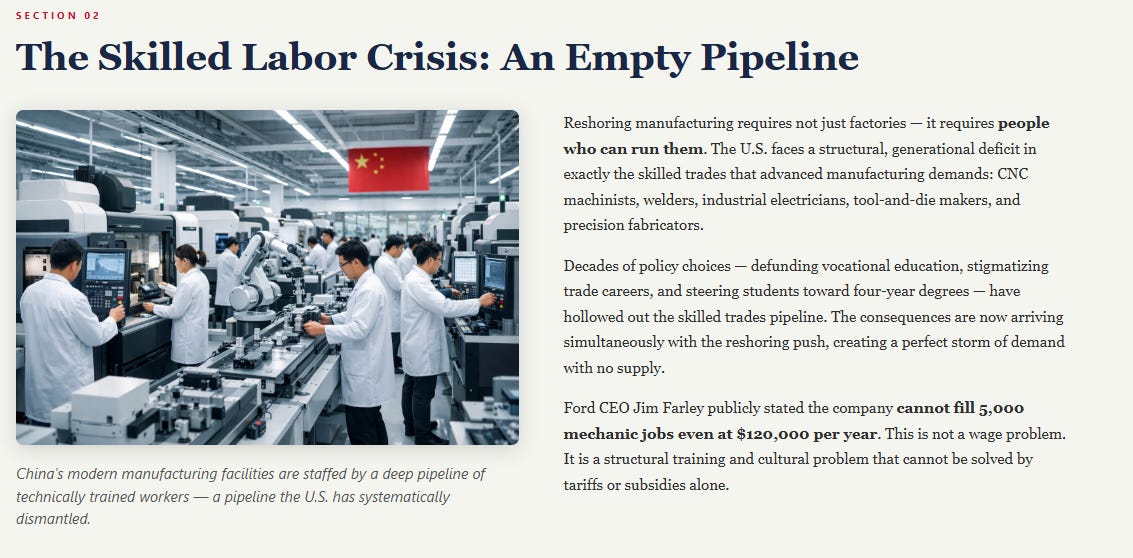

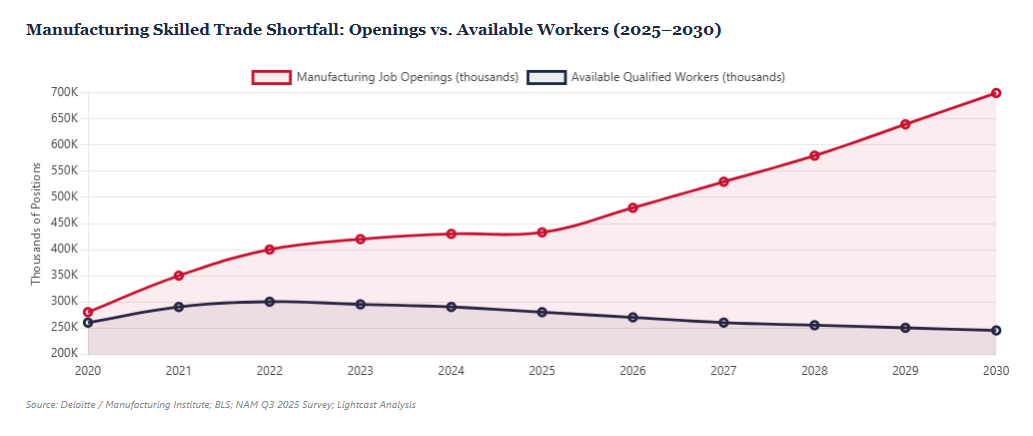

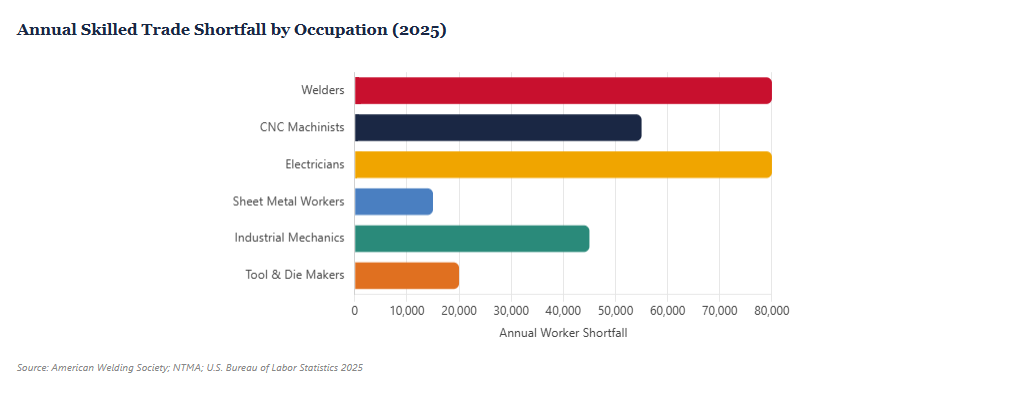

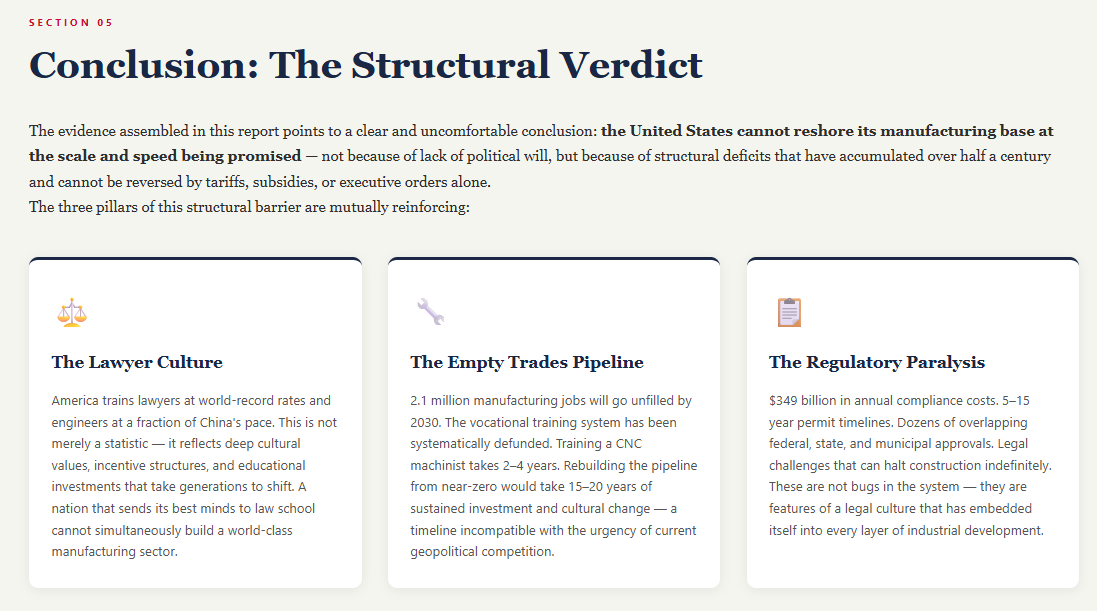

Key Finding: The U.S. skilled trades shortage is structural, not cyclical. Training a CNC machinist to full proficiency takes 2–4 years. Rebuilding the vocational pipeline from near-zero would take a generation. No reshoring initiative can outrun this timeline.

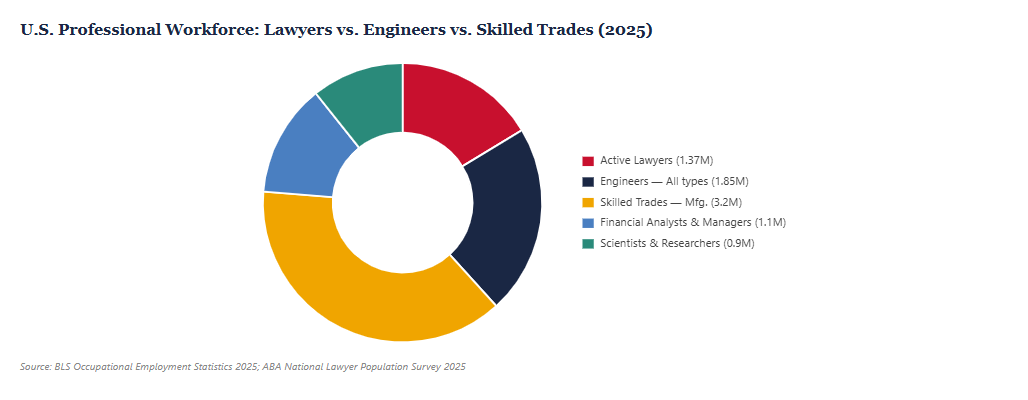

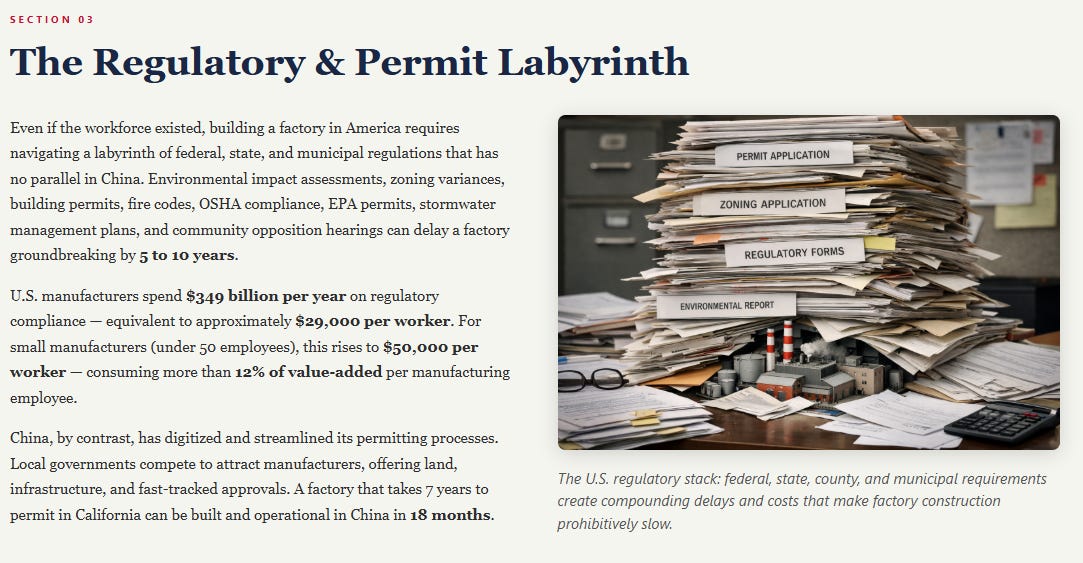

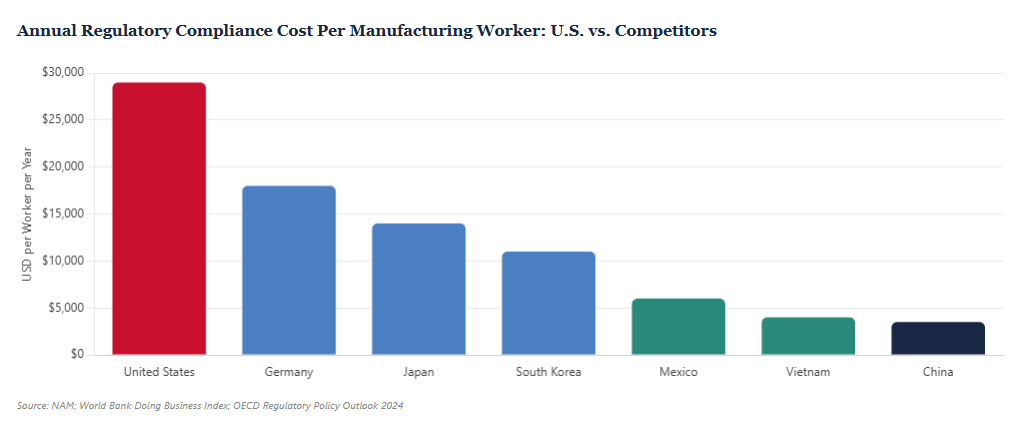

Key Finding: U.S. regulatory compliance costs alone — $29,000 per worker per year — are roughly equivalent to the total annual wages of a Chinese manufacturing worker. This structural cost disadvantage cannot be overcome by tariffs or subsidies without fundamental regulatory reform.

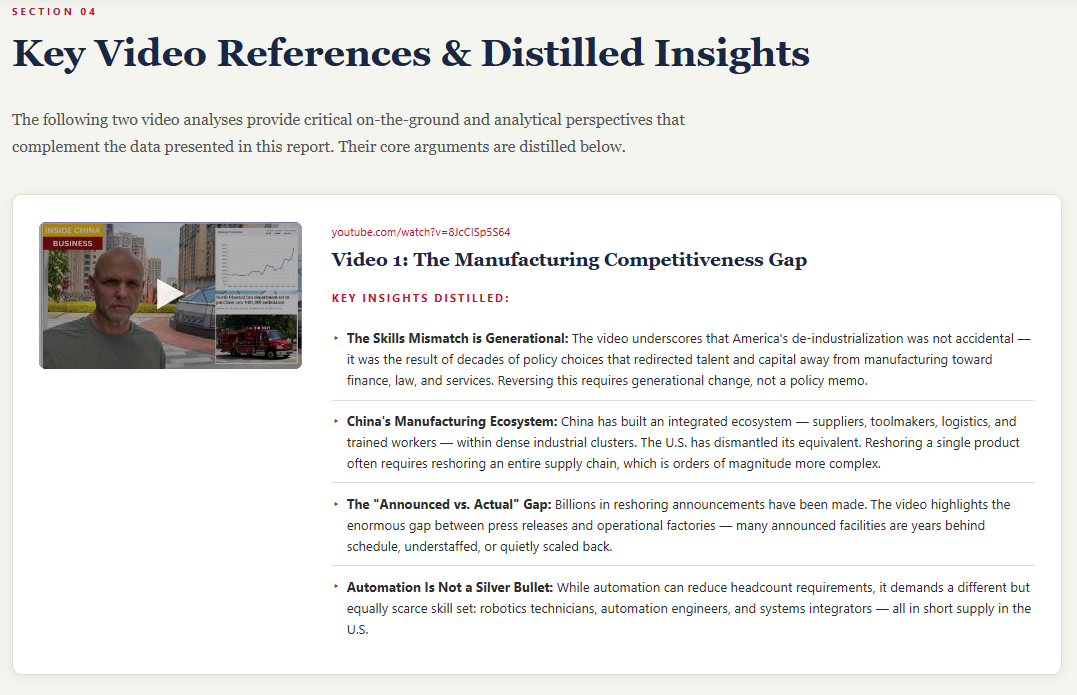

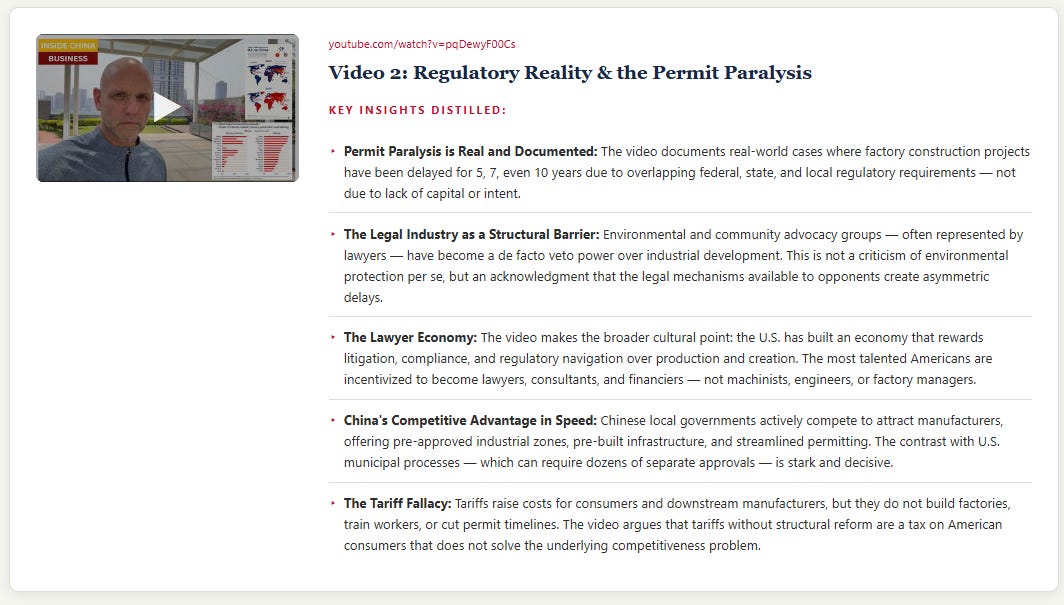

Two Great Videos by Inside China Business:

Combined Takeaway from Both Videos: The reshoring narrative is politically powerful but structurally hollow. Both videos converge on the same conclusion: without a fundamental reorientation of American education, culture, regulatory architecture, and legal incentives, reshoring announcements will remain largely aspirational — generating headlines but not factories, jobs, or industrial capacity.

The reshoring of American manufacturing is not impossible in the long arc of history. But it requires a level of structural reform — in education, regulation, legal culture, and industrial policy — that dwarfs any tariff regime or subsidy package currently on the table. Until the United States is willing to become, once again, a nation that values making things as much as it values litigating about things, the reshoring promise will remain what it currently is: a compelling political narrative disconnected from industrial reality.

Disclaimer: This information and material contained in this post is of a general nature and is intended for educational purposes only. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. This post does not constitute a recommendation or a solicitation or offer of the purchase or sale of securities. Furthermore, this post does not endorse or recommend any tax, legal, or investment related strategy, trading related strategy or model portfolio. The future performance of an investment, trade, strategy or model portfolio cannot be deduced from past performance. As with any investment, trade, strategy or model portfolio, the outcome depends upon many factors including: investment or trading objectives, income, net worth, tax bracket, suitability, risk tolerance, as well as economic and market factors. Economic forecasts set forth may not develop as predicted and there can be no guarantee that investments, trades, strategies or model portfolios will be successful. All information contained in this post has been derived from sources that are deemed to be reliable but not guaranteed.

This is a solid breakdown of the constraints—hard to argue with the labor, cost, and timeline realities.

I do wonder, though, if the framing assumes we’re trying to rebuild the same system we offshored. What’s starting to emerge feels a bit different—more selective reshoring where it matters, combined with automation, energy advantage, and greater control over the flows themselves.

Not so much replication… more reconfiguration.

Curious how you’re thinking about that angle.