Will equities now rhyme the period from 1966 to 1982 on performance?

Will equities go sideways for many years in nominal terms, but go much lower in real terms? What are the implications for investing?

Many are talking about a “stock market crash” or about “asset deflation.” Will it happen? Maybe … but not likely in our world of excessive central bank money printing. Are there historical precedents to what is happening in the equities market? Let’s look at what happened historically, and then assess today’s environment and the implications for investing.

As Mark Twain observes, history never repeats but it often does rhyme. Let’s look at history and see if there any environments or parallels in the past that may be similar to today.

We begin with this long-term chart of the Dow Jones Industrial Average (DJIA), one of the major indices of equities, from 1941 to 1989:

The first thing to notice is the long bull market from 1941 to about 1966.

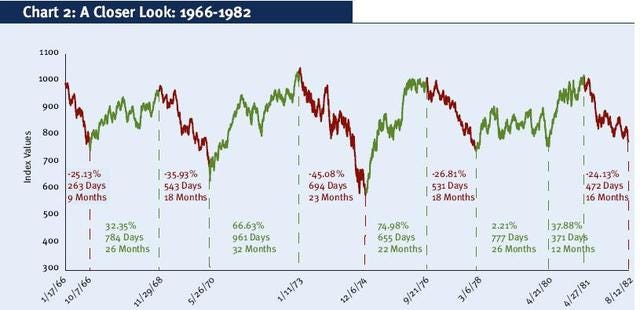

The next thing to notice is the behavior from about 1966 to about 1982 - note the sideways pattern from about 1966 to about 1982 - corresponding to a stagflationary period of time in the economy when economic activity stagnated at the same time general consumer price inflation went higher. So during this 16 years, if you held DJIA equities, you essentially had no nominal gain and no nominal loss - just ending up at the essentially the same level in nominal terms. Here is another view:

Some data during that period indicate:

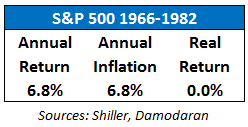

The next thing to notice is how if you include dividends for calculating a total return during the time period, you would have got an annual return of 6.8%. This is in nominal terms. But in inflation-adjusted real terms, your real return would be have 0%. This is the difference between real value versus nominal value.

Real Value = Nominal Value - Inflation Rate

So after noticing this difference between nominal returns and real-terms returns, the study indicates the importance of emphasizing dividend-paying equities during that time-period:

“The Dow went sideways, but the S&P actually earned a respectable 6.8% return in that time. Dividends and earnings also showed relatively healthy annual growth rates. The S&P 500 went from a price level of 92 to 140 so three-quarters of the performance came from dividend payments.” - source link

Another study gives indications of this also:

Current Timeframe

Does it make sense to see parallels of the 1941 to 1982 timeframe to the current timeframe. Well let’s see:

We did have a lengthy long-term rise in equities, especially in the western world where we had the dot.com boom and the recent AI boom, from the late 1990s to recently. As we have noted in our MAA Report, recently about 60% or more of global investable money has gone to the U.S. equity markets and 30% of that into just the Magnificent Seven (MAG7) list - Apple, Microsoft, Google parent Alphabet, Amazon.com, Nvidia, Meta Platforms and Tesla - as a subset of the U.S.-listed technology equities. We can make the analogy of this timeframe of the rise in U.S.-based equities from the late 1990s, comparing it to the rise in the U.S.-based DJIA index of equities from 1941 to 1966.

We have massive government debt and deficits in the western world, relative to the GDP levels - historically governments employ inflation to reduce the burden of government debt, rather than reducing government spending and rather than fiscal prudence.

We do seem to be entering a period of stagflation characterized by stagnant economic activity and rising inflation, especially in the western world countries like the U.S. where the DJIA index of equities is based.

Does that mean the equities may go sideways now for many years, in a manner similar to the 1966 to 1982 stagflationary timeframe?

What are our Most Admired Advisors (MAAs) saying on this?

Are there any of our Most Admired Advisors (MAAs) - group of who we think are the ten best fund managers, asset managers, investment analysts and economists worldwide - providing insight and observations on this nominal vs. real consideration? Link here to our MAA Report - August 2024 Edition. Our MAA Report is like listening in to a board of advisors who we think have the best insights and investment ideas globally.

Let’s consider the words of wisdom from one of our ten MAAs - Dr. Marc Faber, Editor and Publisher of the Gloom Boom Doom Report.

Dr. Marc Faber has explained many times in recent years how economies are dependent today on the high valuations of today’s “highly inflated” equities - which Dr. Faber categorizes as the Magnificent Seven in particular but also to a general extent U.S. equities in general. It is interesting to note that 60% or more of all global investable funds are now in the U.S. markets, even though U.S. GDP is only about 20% of global GDP.. He thinks that there will be a deflation of these “highly inflated” equities. He explains and emphasizes the mechanisms of how central banks can keep these “highly inflated” equities in nominal terms. So instead of seeing a deflation nominally, he thinks we will more likely see the deflation as happening in real-terms. So what that means is for nominal values of the “highly inflated” equities generally may remain elevated in nominal terms, but the real-terms purchasing power generally going lower.

This is a very important point - that the bursting of the so-called asset bubble will likely happen in real-terms (meaning inflation-adjusted or relative to a basket of commodities or relative to gold), and not as much or not much if to any extent in nominal terms. So that we could get the sideways movement in the prices of the equity indices over many years again, especially on equity indices of indebted western world companies.

Here below is a recent podcast discussion in which Dr. Faber gives insight into what happened from 1966 to 1982 when equities went sideways essentially. In inflation-adjusted terms, equities went down 70%. Dr. Faber says a similar phenomenon is happening to wages in the western world countries especially.

Key Lessons and Investing Implications

To a great extent, we assess that our CedarOwl Portfolio - a portfolio of equities emphasizing dividend-paying equities - can help us in investing over a potential stagflationary environment. But what else specifically can we do and how/where can we invest in additionally?

So let’s delve into detailing some of the key lessons from what happened historically and assess how these key lessons can be applied to today’s investing environment - we will detail how we are investing in this environment …